Toggle intro on/off

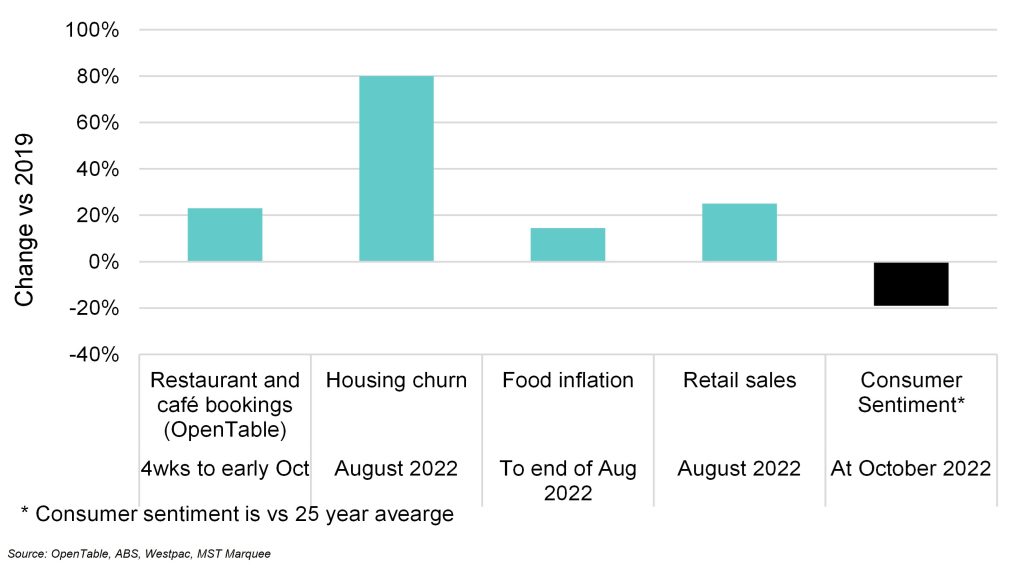

Measuring consumer behaviour vs consumer sentiment

The potential disconnect

12 October 2022

Retail sales for August 2022

Online sales decline

06 October 2022

What correlates with retail sales?

The disconnect between sentiment and spending

26 September 2022

Australian national accounts for June 2021 quarter

Healthy income growth underpins retail spending

01 September 2021

Search result for "" — 628 articles found

Not already a member?

Join now to get all the latest reports in full and stay informed.