Toggle intro on/off

Metcash - Strategy day preview

New CEO’s opportunity to set agenda

15 October 2022

Domino's Pizza - Cost recovery may improve over time

Europe already sluggish

13 October 2022

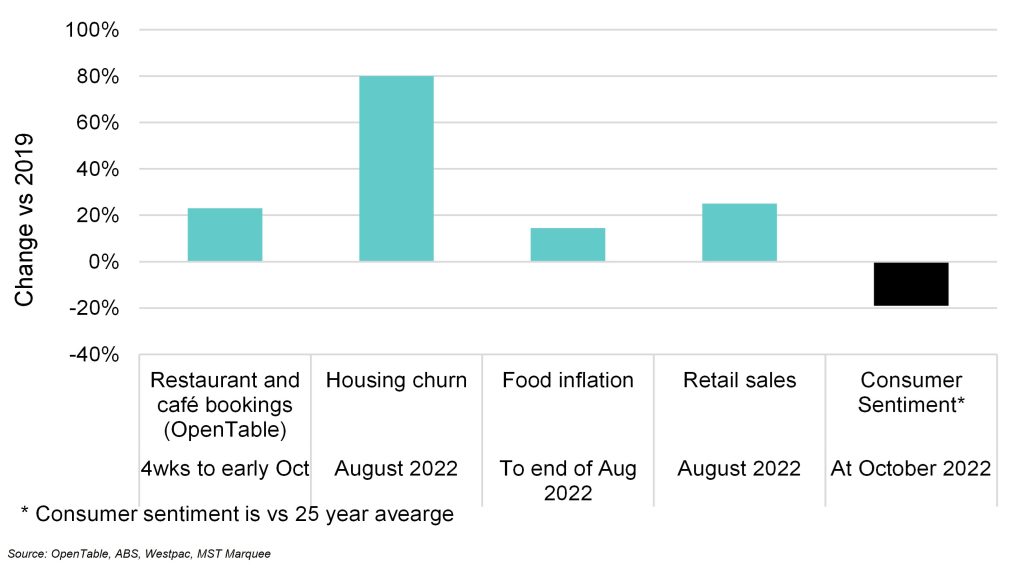

Measuring consumer behaviour vs consumer sentiment

The potential disconnect

12 October 2022

Price Watch Issue 4 - The importance of mix

The overlooked contributor to sales

11 October 2022

Endeavour Group (EDV) How to price gaming risk

The outlook for Endeavour Hotels

10 October 2022

Retail sales for August 2022

Online sales decline

06 October 2022

Premier Investments FY22 result

Pyjama party almost over

01 October 2022

What correlates with retail sales?

The disconnect between sentiment and spending

26 September 2022

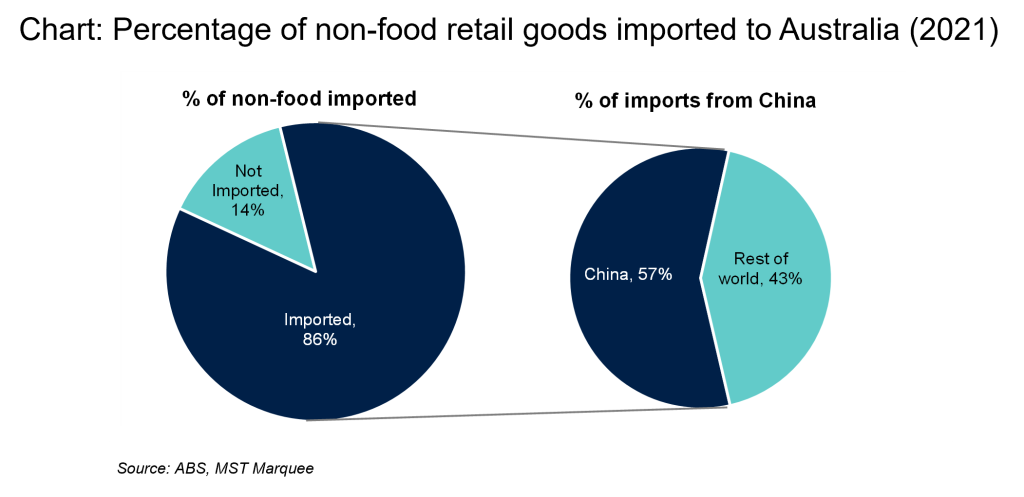

The need to diversify supply chains for Australian retailers

Reliance on China

24 September 2022

Coles Group (COL) Steps away from fuel

Focus on supermarkets and liquor

24 September 2022

Search result for "" — 628 articles found

Not already a member?

Join now to get all the latest reports in full and stay informed.